Behind the Scenes of Mortgage Approval: What Really Happens After You Apply

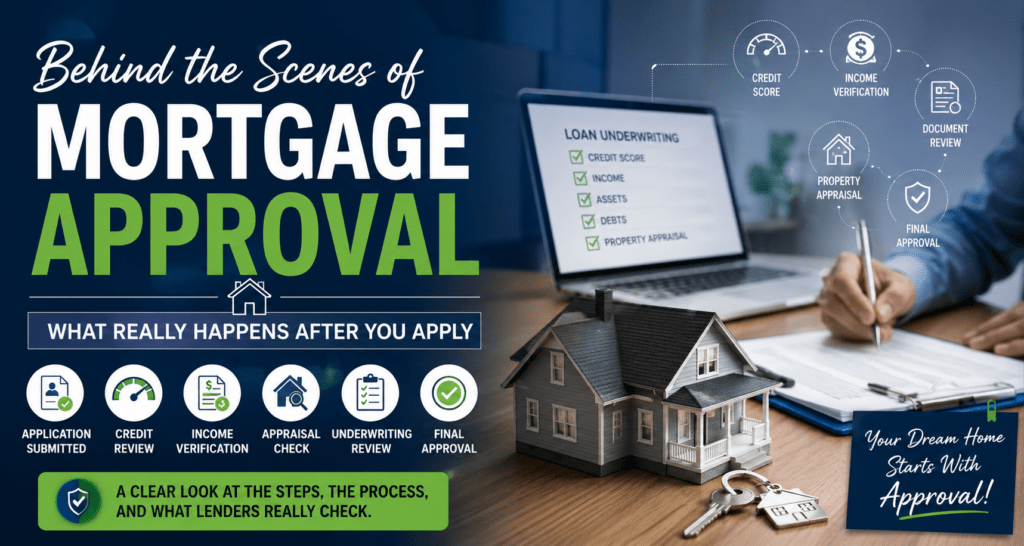

Getting approved for a mortgage may seem simple from the outside, but behind every home loan is a detailed process designed to verify your financial stability and ability to repay the loan. Many buyers submit an application without understanding what lenders actually review during underwriting.

Knowing what happens behind the scenes can help you avoid delays, reduce stress, and improve your chances of approval.

Step 1: Mortgage Pre-Approval Begins

The process usually starts with a mortgage pre-approval. During this stage, lenders evaluate your:

- Income

- Employment history

- Credit score

- Debt obligations

- Bank statements

Pre-approval gives buyers a realistic budget and shows sellers they are serious and financially qualified.

Step 2: Credit Review

One of the first things lenders check is your credit profile.

What Lenders Look For

- Credit score

- Payment history

- Credit utilization

- Collections or late payments

- Bankruptcies or foreclosures

- Length of credit history

Higher credit scores often lead to better interest rates and loan terms. Even small improvements in credit can save thousands over the life of a mortgage.

Step 3: Income Verification

Lenders need proof that borrowers have stable and reliable income.

Common Income Documents

- Pay stubs

- W-2 forms

- Tax returns

- Bank statements

- Profit and loss statements for self-employed borrowers

The goal is to verify that income is consistent enough to support monthly mortgage payments.

Step 4: Debt-to-Income Ratio Analysis

Your debt-to-income ratio (DTI) compares monthly debt payments to gross monthly income.

Lenders review:

- Car loans

- Credit cards

- Student loans

- Personal loans

- Existing mortgages

A lower DTI improves approval chances because it shows you are not financially overextended.

Step 5: Property Appraisal

Once a home is selected, the lender orders an appraisal.

Why the Appraisal Matters

The appraisal confirms:

- The home’s market value

- Property condition

- Comparable home prices nearby

Lenders want to ensure the property is worth the loan amount being requested.

If the appraisal comes in low, buyers may need to renegotiate the purchase price or increase the down payment.

Step 6: Underwriting Review

This is the most important stage behind the scenes.

Mortgage underwriters carefully review:

- Credit reports

- Income documents

- Employment history

- Assets

- Appraisal reports

- Loan program guidelines

The underwriter determines whether the loan meets all lending requirements.

This stage may involve additional document requests known as “conditions.”

Step 7: Conditional Approval

Many borrowers receive conditional approval before final approval.

Common conditions include:

- Updated bank statements

- Additional pay stubs

- Explanation letters for large deposits

- Verification of employment

Responding quickly to these requests helps prevent closing delays.

Step 8: Final Loan Approval

Once all conditions are cleared, the lender issues final approval.

At this point:

- Loan documents are prepared

- Closing disclosures are sent

- Closing dates are confirmed

Buyers should avoid:

- Opening new credit accounts

- Making large purchases

- Changing jobs before closing

Even last-minute financial changes can affect final approval.

Step 9: Closing Day

Closing is the final step where ownership officially transfers to the buyer.

During closing:

- Loan documents are signed

- Closing costs are paid

- Funds are transferred

- Keys are delivered

After closing, the mortgage becomes active and monthly payments begin according to the loan agreement.

Common Reasons Mortgage Approvals Get Delayed

Incomplete Documentation

Missing paperwork is one of the biggest causes of delays.

Credit Changes

New debts or missed payments during the process can create problems.

Employment Changes

Switching jobs may require additional verification.

Appraisal Issues

Low appraisals can delay or impact loan approval.

Large Bank Deposits

Unverified deposits often trigger underwriting questions.

Tips to Make Mortgage Approval Easier

Keep Financial Records Organized

Prepare tax returns, pay stubs, and bank statements early.

Avoid Major Financial Changes

Do not finance vehicles or make large purchases before closing.

Maintain Stable Employment

Consistency matters during underwriting.

Improve Your Credit Score

Pay bills on time and reduce credit card balances.

Work with Experienced Mortgage Professionals

A knowledgeable loan expert can help identify issues before they become problems.

Final Thoughts

Mortgage approval is much more than filling out an application. Behind the scenes, lenders carefully evaluate credit, income, assets, debt, and property value to ensure borrowers are financially prepared for homeownership.

Understanding the process can help buyers move through approval faster and with greater confidence.

For expert mortgage guidance and personalized loan solutions, visit Official Angelo Christian