FHA vs Conventional Loans: Which One Is Better in 2026?

Buying a home in 2026 comes with one big question: should you choose an FHA loan or a conventional loan? The answer depends on your credit score, down payment, income stability, and long-term financial goals.

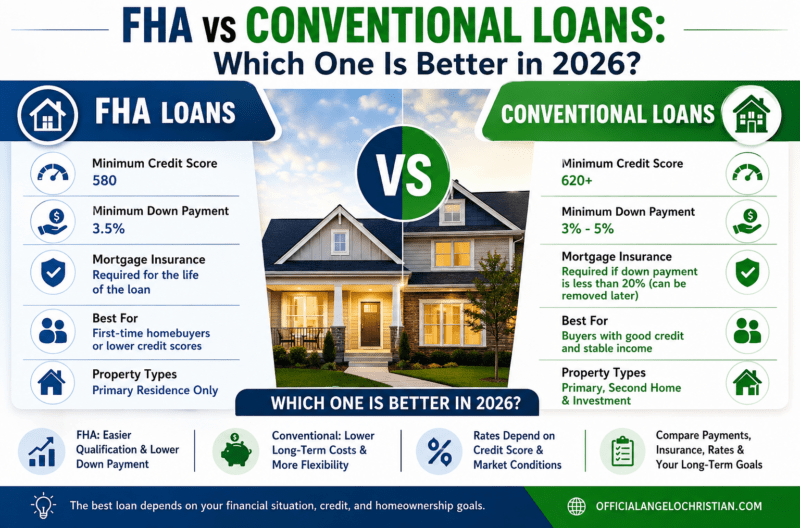

Both loan types help buyers become homeowners, but they work very differently when it comes to qualification requirements, mortgage insurance, and total loan cost. FHA loans are designed to help buyers with lower credit scores or limited savings, while conventional loans reward borrowers with stronger financial profiles.

What Is an FHA Loan?

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration. These loans are popular among first-time homebuyers because they offer flexible qualification requirements and lower credit score standards.

FHA Loan Highlights

- Minimum credit score: typically 580

- Minimum down payment: 3.5%

- Easier approval process

- Higher debt-to-income flexibility

- Mortgage insurance required

FHA loans are especially helpful for borrowers rebuilding credit or those who may not qualify for conventional financing.

What Is a Conventional Loan?

A conventional loan is not backed by the government. Instead, it follows guidelines set by private lenders and agencies like Fannie Mae and Freddie Mac.

These loans usually require stronger credit and financial stability but can save borrowers significant money over time through lower mortgage insurance costs.

Conventional Loan Highlights

- Minimum credit score: usually 620+

- Down payment as low as 3%

- Lower long-term borrowing costs

- PMI can eventually be removed

- Better rates for high-credit borrowers

FHA vs Conventional Loan Comparison (2026)

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Credit Score | 580 (sometimes lower with larger down payment) | Usually 620+ |

| Minimum Down Payment | 3.5% | 3%–5% |

| Mortgage Insurance | Required on all FHA loans | Required only below 20% down |

| Mortgage Insurance Removal | Often lasts for life of loan | Can be removed after reaching equity |

| Debt-to-Income Flexibility | More flexible | Stricter |

| Best For | Lower credit borrowers | Strong credit borrowers |

| Property Types | Primary residence only | Primary, second homes, investments |

Mortgage Insurance: The Biggest Difference

One of the most important differences between FHA and conventional loans is mortgage insurance.

FHA Mortgage Insurance (MIP)

FHA loans require:

- Upfront mortgage insurance premium

- Monthly mortgage insurance payments

If your down payment is under 10%, the insurance may remain for the life of the loan.

Conventional Mortgage Insurance (PMI)

Conventional loans only require PMI if you put down less than 20%. The biggest advantage is that PMI can be removed once enough equity is built in the property.

This is why many buyers with higher credit scores prefer conventional financing long term.

Which Loan Has Better Interest Rates in 2026?

Interest rates vary based on:

- Credit score

- Debt-to-income ratio

- Loan amount

- Market conditions

FHA loans may sometimes offer competitive rates for lower-credit borrowers, but conventional loans often become cheaper overall for buyers with strong credit because of lower mortgage insurance costs.

FHA Loan Pros

Easier Qualification

Borrowers with lower credit scores often qualify more easily.

Lower Down Payment

Only 3.5% down is required in many cases.

Flexible Credit History

Past bankruptcies or credit challenges may be accepted faster than with conventional loans.

FHA Loan Cons

Lifetime Mortgage Insurance

This can increase total loan cost significantly.

Lower Loan Limits

FHA loans may not work well for luxury homes.

Primary Residence Only

Cannot usually be used for vacation or investment properties.

Conventional Loan Pros

Lower Long-Term Cost

PMI can eventually disappear.

Better for High Credit Borrowers

Excellent credit can unlock lower rates.

More Property Flexibility

Can finance investment properties and second homes.

Conventional Loan Cons

Stricter Approval Standards

Higher credit and income stability are important.

Harder for First-Time Buyers with Weak Credit

Some buyers may struggle to qualify.

Which Loan Is Better in 2026?

FHA Loan Is Better If:

- Your credit score is below 680

- You have limited savings

- You need flexible qualification standards

- You are a first-time homebuyer

Conventional Loan Is Better If:

- Your credit score is strong

- You can afford a larger down payment

- You want lower long-term costs

- You plan to build equity and remove PMI

Final Thoughts

There is no one-size-fits-all answer when choosing between FHA and conventional loans in 2026. FHA loans help buyers enter the market faster with easier qualification standards, while conventional loans often provide better long-term savings for financially strong borrowers.

The smartest move is to compare:

- Monthly payment

- Mortgage insurance

- Interest rate

- Closing costs

- Long-term ownership goals

Before choosing a mortgage, get pre-approved and review multiple loan scenarios to find the option that truly fits your financial future.

For personalized mortgage solutions and loan guidance, visit Official Angelo Christian